My Top 4 Stock Picks for 2025

Happy new Year! I thought i would have a go with my top 4 picks for 2025. These are on the FTSE 100 & FTSE 250.

Dear reader,

As the year draws in and we look towards 2025, I thought I would have a little fun and place predictions on a couple of stocks I believe might do well. I won’t bore you to death with endless explanations but rather state why I believe this is the case. Please note this is only my opinion and this is not advice.

Phoenix Group Holdings PLC (FTSE 100)

Share price: 510.00 p (31/12/2024)

Sector: Insurance

P/E: 15.32

Just taking a look on the outside first, this is one of the highest paying dividend stocks on the FTSE 100, currently the yield is c.10% (Schroders 6.64%). The 5 year low of the share price was around £4.45 and today sits around £5.10 (only a 14% increase of 5 year lows).

Taking a look at their most recent results:

Positives:

Operating cash generation up 19% to £647m; confident in hitting 2024 cash targets.

Resilient £3.5bn Solvency II surplus and 168% capital coverage ratio.

Adjusted operating profit rose 15% to £360m; contractual service margin grew 10%.

Workplace net fund flows increased 83% to £3.3bn; strong new product launches.

£250m debt repaid; progress toward £50m cost savings by 2024.

“delivered 19% growth in Operating Cash Generation and remitted total cash generation of £950 million in the first half. We have generated 3%pts of recurring Solvency II capital and our resilient balance sheet has enabled us to repay £250 million of debt and to invest in our business”.1

Negatives:

Solvency II surplus down from £3.9bn to £3.5bn due to debt repayment and investments.

IFRS loss widened to £(646)m, hit by adverse economic variances.

Shareholders' equity dropped to £1.8bn from £2.7bn.

Annuity premiums fell to £1.7bn from £3.2bn.

SunLife sale process discontinued amid market uncertainty.

Phoenix Group is a solid company that’s consistently improving its business. They’ve made great progress paying down £250m of debt and have launched "Future Growth Capital," a private markets investment manager in partnership with Schroders – a smart move that shows they’re focused on growth.

I think putting the sale of SunLife on hold was the right call. It shows they’re not under pressure to sell and can take their time to maximise its value. This is a stock I’m happy to hold, collecting the dividend while the company continues to move in the right direction.

BP (FTSE 100)

Share price: £3.85 (30/12/2024)

Sector: Oil & Gas

P.E: 7.45

BP has faced challenges recently, with several factors contributing to its decline. The UK government's commitment to banning new petrol and diesel car sales by 2030, alongside a global slowdown in economic activity and reduced oil demand, also the Middle East, have all negatively impacted the company. As a result, BP's share price has fallen from its recent highs, and its third-quarter profit dropped 30% in 2024, largely due to weaker refining margins and lower oil prices

However…..

“Free cash flow more than doubled to $4.4bn, reflecting improved cash generation from operations and lower capital expenditure. Net debt fell from $23.7bn to $22.6bn.”2

I'm also optimistic about BP, trading near year lows and paying a dividend of 6%. BP is planning to save around $2bn in costs by the end of 2026. The business has been growing its biogas, electric vehicle charging, and renewables sectors to help future-proof itself.

The US Energy Information Administration (EIA) has revised up its forecast for crude oil prices by $2 per barrel through the end of next year due to the expectations of a higher global oil demand growth in 2025.

BP offers strong dividends and solid cash generation, though its growing debt is a concern. Despite this, I believe BP can overcome the challenges, and at current prices, it represents good value for money. For comparison, Chevron has a P/E of 12.59 and ConocoPhillips a P/E of 11.32. I’m confident BP can improve, and I’m comfortable with the dividend yield.

Persimmon PLC (FTSE 100)

Share price: £11.98 (31/12/2024)

Sector: House Building

P.E: 14.83

It’s been a rough few months for housebuilders all round, and Persimmon is no different. But let’s start with why I think they’re set to do well. The government’s target for building new homes is massive – we’re talking 1.5 million new homes over the next five years!

“Now it faces the task of meeting this target; doing so will require a rate of completing new homes not seen since the 1960s.”3

As the second-largest residential property developer, Persimmon focuses on lower-priced new builds – exactly where the government is aiming to implement its ambitious housing target. As a result, the company’s order book has grown by 17% compared to the previous year.

There are some downsides. Rising costs are worrying investors, but Persimmon has reassured them by working closely with their supply chain to manage expenses. The rise in interest rates has weakened demand for new homes, resulting in a 67% drop in EPS. With bad news from the budget and ongoing inflation, it may seem like a challenging situation.

That said, I view Persimmon as a long-term hold. With a price-to-earnings growth ratio of around 0.8 and a price-to-book ratio of 1.2, there’s a solid margin of safety, suggesting the company is oversold. Given the continued demand for housing and efforts to get people onto the property ladder, if Persimmon can control its costs, I believe the company has the potential to perform well over time.

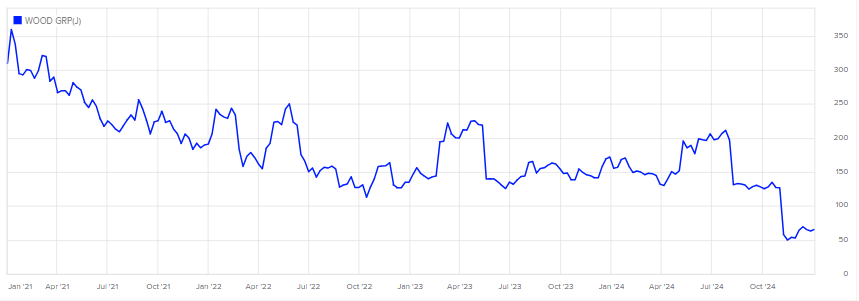

John Wood Group (FTSE 250)

Share price: 64.00 p (30/12/2024)

Sector: Energy Equipment and Services

P.E: -0.53

I'm optimistic about JW for a few reasons. A drop from £1.24 to a low of 49p in one day (around -60%) seems excessive to me. While there has been some recovery, the share price now sits at 64p.

The company has secured several notable contracts, including a six-year agreement with Shell to support the world’s largest floating offshore LNG facility in Australia and a three-year deal to operate Freepoint Eco-Systems' advanced recycling facility. Other highlights include a $40 million engineering design project for a sustainable packaging plant in Singapore and a seven-year, $200 million master service agreement with BC Hydro to modernize and expand British Columbia's electric grid.

There are risks. One of the major reasons for the share price crash was the announcement of an urgent independent review of its books.

“Wood announced write-offs of almost $1bn in August after deciding to exit certain types of work and recognise costs related to legacy acquisitions, pushing the company into an operating loss of $899mn in the six months to June”4

As stated above, the write-offs were significant, pushing the business into a substantial loss. Furthermore, the company was already experiencing difficulties, including two failed takeover bids. I have to admit the business is going through tough times, but I believe the review won’t be as bad as the market expects. With these large wins and more to come, the business can (could) turn itself around. This is one high risk even for me!

Happy new year!

I hope you all have great new year and are ready for 2025.

I’d love to hear what you think!

Do you agree with my picks for 2025, or do you have your own favourites? Are there any stocks you’re particularly excited about for the year ahead? Drop a comment below, or feel free to reach out with your thoughts—I’m keen to hear your views!

Thanks for reading,

Ollz

The information provided in this article is for informational purposes only and reflects my personal opinions and analyses. It should not be considered financial advice or a recommendation to buy or sell any securities. Investing in the stock market involves risks, and past performance is not indicative of future results. Readers are encouraged to conduct their own research and consult with a qualified financial advisor before making any investment decisions. I do not assume any responsibility for any financial losses or consequences that may arise from reliance on the information provided herein.

https://www.thephoenixgroup.com/news-views/2024-half-year-results/

https://www.hl.co.uk/shares/share-research/bp-mixed-results-but-strong-cashflows-underpin-more-buybacks

https://www.instituteforgovernment.org.uk/publication/how-government-build-more-homes#:~:text=It%20has%20set%20an%20ambitious,affordable%20housebuilding%20in%20a%20generation%E2%80%9D.

https://www.ft.com/content/45b79283-07eb-4e53-bff3-b23531e93d20