Dear reader,

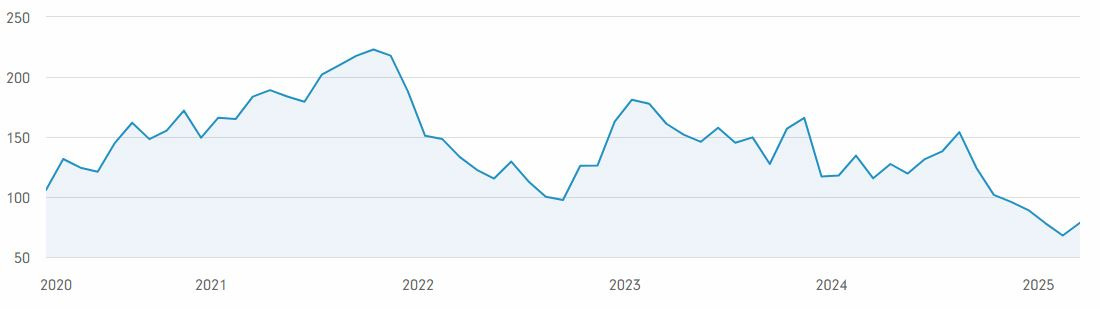

This week, we’re taking a closer look at JD Sports — and why I’m treading carefully. At first glance, the stock looks like a bargain: the share price is hovering near five-year lows, the P/E ratio sits at just 12.9, and management has a bold turnaround plan that includes opening a wave of new stores.

But could it be a value trap? In this article, we’ll dig into the numbers, weigh the risks and rewards, and run a valuation to decide whether JD Sports deserves a spot in the fund.

Trying to Grow Too Fast?

JD sports under CEO Regis Schultz has set the way for growth it would seem. In 2023, JD Sports unveiled a five-year strategic plan built around four key pillars:

JD Brand First

Complementary Concepts

Beyond Physical Retail

People, Partners, and Communities

If you walk into a JD Sports store, I think you would expect to see brands like NIKE, Adidas and Under Armour. However, it looks like in the background JD have been growing their private label brands and “currently has around 60 own-label brands, including Supply & Demand, Pink Soda and Cecil Gee”. What's more, the private label product sales represent around “5% of annual apparel sales”.

Its not just stores, JD has a strong online market place. In 2024 around 22% of sales were online. Noteworthy to add that JD sports is taking their cybersecurity more seriously. In one of my most recent articles we explored the financial impacts that cyber attacks are having on M&S and its share price:

In 2023 JD sports was hit by a cyber attack, “The attack related to online orders placed”. The costs were not too significant compared to a current cyber attack on M&S which wiped almost £700 m off the retailers valuation!

JD has ventured into a totaly new segment, Gyms! Upon doing more research on their gyms (first one opened in 2014) they seem to be battling the cheaper market with the Gym group with a difference in the price per month of around £2. Positive news, as I think this reaches their clients who are 16-24 year olds and unlikely to afford a David Loyds membership of £130 a month!

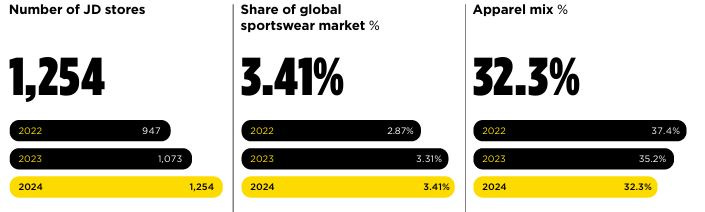

The US is now the largest single-country market for JD Sports, with 2,241 stores — compare this to the UK's 432 stores! JD views the US as a high-growth, high-potential market. They plan to open 200–250 new stores annually in the US. The US also has a loyalty programme with 5.1 million active JD Status members, helping to create brand loyalty.

The Financials

Income Statement:

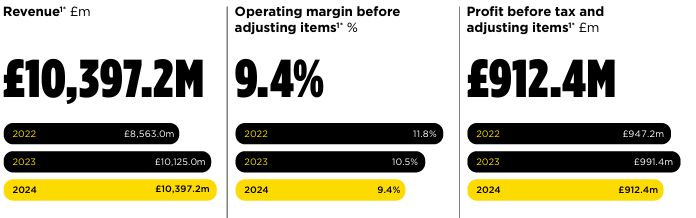

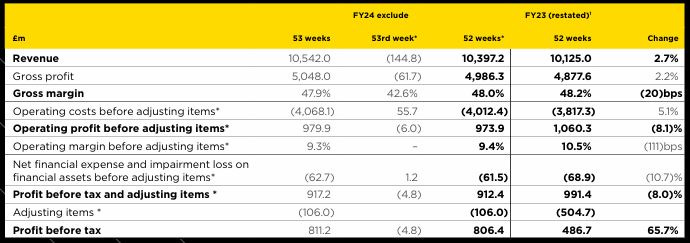

JD Sports generated revenue of £10,397.2 million in 2024, an increase of 2.7% year-on-year on a comparable 52-week basis. Operating profit rose to £927.2 million, up 15.0%, while profit before tax and adjusting items declined by 7.5% to £917.2 million, reflecting a more promotional and competitive trading environment — particularly in North America and Europe during peak periods. Statutory profit before tax was £811.2 million, a 66.7% increase, primarily due to a lower level of adjusting items compared to the prior year. Basic earnings per share rose to 10.45p, up 186.3%.

Balance Sheet:

The group ended the year with net cash (before lease liabilities) of £1.0 billion, indicating a strong liquidity position. Lease liabilities — mainly related to store leases under IFRS 16 — stood at £2.3 billion. Total borrowings (excluding lease liabilities) were negligible at £0.2 million, while total equity increased to £2.7 billion, supported by retained earnings and continued profitability. The company’s asset base expanded through ongoing investment in new store openings and digital infrastructure. However, the annual report highlights significant deficiencies in internal controls and financial processes, which complicated the year-end reporting. Management has outlined plans for remediation.

Cash Flow:

JD Sports remained highly cash-generative in 2024, with operating cash flow supporting continued investment in organic growth, including the opening of 216 new JD stores. Capital expenditure was directed towards store expansion, digital platforms, and complementary retail concepts. The group’s strong cash position provides flexibility for future growth initiatives and potential acquisitions, while also supporting working capital needs in a challenging retail environment.

Ownership Strucutre:

This is particularly interesting given that Pentland Group Ltd, a private business, owns 51.6% of JD Sports and ultimately controls the group’s strategic direction and decisions. Other notable institutional investors include Fidelity Management & Research (4.5%), BlackRock Investment Management (3.3%), Norges Bank (2.8%), and The Vanguard Group (1.7%).

Having a single majority shareholder like Pentland can be a double-edged sword. On the one hand, it often brings stability and a long-term strategic vision, as reflected in JD Sports’ consistent international expansion and brand development. On the other hand, majority control can present governance risks if the controlling shareholder’s interests diverge from those of minority investors. For example, Sports Direct (now Frasers Group) under Mike Ashley faced criticism for governance practices perceived to prioritise founder interests over shareholder value. In contrast, LVMH has flourished under family control, maintaining brand integrity and delivering sustained growth. Ultimately, the impact of majority ownership depends on the alignment between the controlling party and minority shareholders, as well as the overall strength of governance structures.

Unfortunate Competitors?

JD Sports finds itself in a challenging position. It acts as a middleman, selling popular third-party brands like Nike and Adidas, while simultaneously competing with major retailers such as Foot Locker and Frasers Group. The sector is highly competitive, and JD must navigate it carefully.

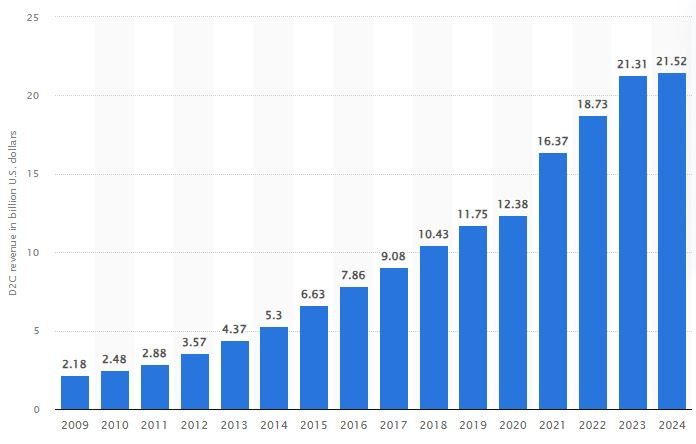

A growing concern is the rise of direct-to-consumer (D2C) strategies by brands like Nike and Adidas. Both companies are increasingly focusing on selling directly to consumers through their own channels, which could marginalise retailers like JD. As the graph below shows, Nike’s D2C revenue has grown rapidly in recent years—a trend that could significantly reshape the retail landscape.

Moreover, if it’s a bad year for Nike, it’s likely to be a bad year for JD Sports. Approximately 50% of JD’s revenue comes from Nike, making it heavily reliant on the brand. Being Nike’s number one global partner may sound like a strength, but it comes at a price—namely, reduced bargaining power. If Nike decides to increase costs or change terms, JD has little room for negotiation. Sure, JD could refuse, but the consequences of not selling Nike products would be significant.

This dependency is so strong that JD’s share price often reacts to Nike’s performance. As This is Money reported:

“The self-styled King of Trainers took a kicking, losing 5.4 per cent, or 6.85p, to 119.5p, as Nike warned that its 2025 revenues would be lower than expected.”

Risks and Rewards:

JD Sports presents investors with a mix of opportunities and risks. While the company has solidified its position as a global sportswear giant, with FY2024 revenues of £10.5 billion—an increase of 2.7% year-on-year—it faces significant challenges in its domestic market. Like-for-like sales in the UK and Republic of Ireland declined by 7% in the first quarter of FY25, reflecting weak discretionary spending amid ongoing cost-of-living pressures and high interest rates. Despite this, JD remains focused on achieving over £1 billion in EBIT by FY2028, with international expansion and disciplined cost control as key pillars of its strategy. This includes a £100 million reduction in administrative expenses over the past year. The company’s recent acquisition of Hibbett, a major US retailer, is expected to strengthen its North American presence—now the largest contributor to group profit—and could provide a competitive edge if the integration is successful.

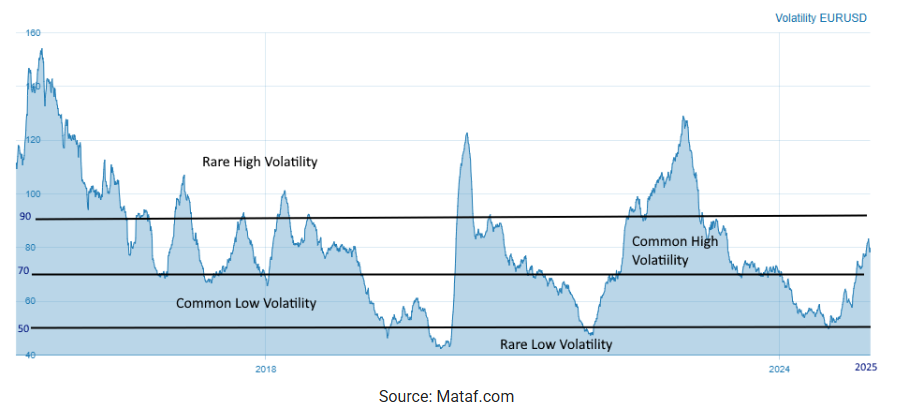

From a broader macroeconomic perspective, investors must balance JD’s global ambitions with regional economic headwinds. The company stands to benefit from the structural shift towards athleisure and premium casualwear, but it remains heavily dependent on key brand partners like Nike and Adidas to maintain its product differentiation. Any changes in wholesale strategies from these brands—such as an increased focus on direct-to-consumer channels—could impact JD’s margins. Additionally, currency volatility, particularly in the US dollar and euro, poses a further risk, given JD’s extensive international operations.

EURUSD Volatility:

Meanwhile, the Asia Pacific region remains loss-making, underscoring the execution risks in less mature markets. For UK-based investors, JD's current valuation—around 10x forward earnings—may appear attractive, especially when compared to historical averages. However, investor sentiment could remain fragile unless there is a clear recovery in domestic sales and a successful delivery on overseas growth targets.

Aqusitions, JD status and JD Gyms

JD Sports' acquisitive strategy continues to reshape its global footprint. In FY25, the Group added over 1,400 stores through the acquisitions of US-based Hibbett and European retailer Courir, bringing its total store estate across all brands to 4,850. These acquisitions help JD expand its reach into new customer demographics—Hibbett into US community retail and Courir into Europe's female consumer base. Management expects a 10% uplift in FY26 revenue from these acquisitions, supported by 150 new store openings and 100 refurbishments. However, the company anticipates lower like-for-like revenue growth this year, suggesting that inorganic expansion may be offsetting weaker underlying demand—particularly in the UK, where Q4 FY25 like-for-like sales were down 2.5%.

JD STATUS, the Group’s digital loyalty platform, is a key tool for driving customer engagement. By FY24, it had 5.1 million active users in the US and 800,000 app downloads in the UK, with reported average transaction values 40% higher among members. While early usage metrics are promising, the commercial impact remains undisclosed, and the European rollout is still in its early stages. JD Gyms, which operates 80+ sites in the UK, provides another growth opportunity. Positioned between budget and mid-market competitors like PureGym, it generates recurring revenue and aligns with JD’s core 16-24 demographic. However, the segment faces challenges, including cost inflation, competitive pricing, and a slow recovery in consumer spending outside major cities—headwinds that may limit near-term profitability.

JD Sports fair value assessment:

Conservative Forward P/E Valuation (P/E = 10):

If we apply a forward P/E ratio of 10, which is a cautious approach reflecting current market uncertainties and sector risks, the fair value calculation is:

With JD Sports’ current share price around 81.2p, this suggests the shares could be undervalued, offering potential upside if the business delivers stable earnings.

Market-Implied Forward P/E Valuation:

Alternatively, we can infer what the market expects by dividing the current share price by the consensus forward EPS estimate. With the share price at 81.2p and consensus FY2025 EPS estimates around 13.67p (based on analyst forecasts and implied from the current price), the market-implied forward P/E is:

Conclusion: Why JD Sports Remains on My Radar

To wrap up, I continue to like JD Sports as a business. Admittedly, I tend to focus on its UK operations and US expansion when evaluating the company. In the UK, it’s clear that retail remains challenging—only a handful of businesses are managing to navigate the environment successfully. One such example is Next plc, which, while targeting a different demographic, offers an interesting point of comparison.

Next recently reported record pre-tax profits of £1 billion (March 2025), with total sales up 8.2% and full-price sales up 5.8%. Like JD, it operates across both physical stores and online channels. Crucially, Next has successfully scaled its own brands while also offering third-party products—a strategy I’d like to see JD Sports lean into more aggressively.

JD Sports has the potential to perform well across both the UK and US markets. The long-term opportunity is compelling. From a valuation standpoint, however, timing matters. The share price has rallied 27% over the past month, and while 80p could still be considered attractive, I’m currently more inclined to accumulate shares trading near their five-year lows—around the 70p level. That said, this view is fluid. In today’s market, so many variables are in play that flexibility is essential.

JD isn’t a conviction buy just yet, but it’s firmly on the watchlist—and could soon earn a place in the fund.

Thanks for reading, Ollz!

The information provided in this article is for informational purposes only and represents my personal opinions and analysis. It should not be construed as financial advice or a recommendation to buy or sell any securities. Investing in the stock market carries risks, and past performance is not necessarily indicative of future results. Readers are strongly encouraged to carry out their own research and seek advice from a qualified financial advisor before making any investment decisions. I do not accept any responsibility for any financial losses or consequences that may arise from reliance on the information presented in this article.

For the UK, the working portion of the target 16-24 year old demographic will be benefiting from the large increase in the minimum wage, and are probably shielded from some cost increases, such as rising energy and council tax, as most will be living with parents. New holder (before reading this article).

It’s an interesting point. That said, I’m less optimistic about the extent to which price hikes from brands like Adidas and Nike can be absorbed by JD and ultimately passed on to the customer. As I mentioned in the article, I’d really like to see stronger growth in JD’s own-brand offering — something along the lines of what we’ve seen with Next plc