Greggs -13%, Bytes -31%: What’s Happening?

A closer look at the reasons behind today’s sharp share price moves

Dear reader,

It’s been an interesting day with significant movement across the FTSE. I’m writing this article because the recent news around Greggs and Bytes deserves more detailed exploration than brief notes allow. Both companies are well-known constituents of the FTSE 250, though they operate in very different sectors. In this article, I’ll review their latest results and try to unpack what triggered such sharp share price drops in a single day.

Greggs PLC -13% (02/07/2025)

P/E Ratio: 11.29

Price/Book: 3.51

Dividend (Yield): 4.12%

EPS: 1.51

Sales Growth

Total sales rose 6.9% to £1.03 billion in the 26 weeks to 28 June, supported by both store expansion and existing shop performance. Like-for-like (LFL) sales – which exclude the benefit of new store openings – increased by 2.6%. That marks a meaningful slowdown compared to the prior year, when LFLs in Q2 2024 stood at 6.5%.

Management highlighted that June’s very warm weather led to lower footfall, particularly in city centre and high street locations. While demand for cold drinks rose, it wasn’t enough to offset weaker demand for core food-to-go ranges.

Reports have come out that theft at Greggs is growing! “Greggs will move its self-serve food and drinks to behind the counter to stamp out shoplifting at the High Street bakery. The company is trialling the measure at a handful of stores which, it said, are "exposed to higher levels of anti-social behaviour". Is it the hot weather or is it the levels of theft at Greggs which are hurting the business?

Store Rollout

Greggs opened 87 new shops in the period and closed 56, resulting in a net increase of 31 locations. It now operates 2,649 shops in total and remains on track to deliver 140–150 net openings this year. Alongside that, the company completed 108 refurbishments in H1 – front-loading investment and pushing up short-term costs.

While this programme supports the longer-term strategy to broaden access and improve customer experience, it places pressure on operating margins, especially when same-store sales are slowing. These dynamics have led management to guide that full-year operating profit will likely be “modestly below” 2024’s level.

The Bigger Picture

One thing I like to do is my own due diligence — and it’s even easier when doing due diligence at Greggs. What do I notice? Well, just the number of people! It always seems busy in the mornings, and lunchtime is no different. In my recent article on Greggs, we discussed how the business is, and wants to be, expanding into offering different meals later in the day. I imagine they’re looking at the likes of McDonald’s, which offers food for all times of the day.

The business benefits from strong brand loyalty, an affordable product range, and growing relevance across new channels — whether through retail parks, forecourts, or delivery platforms. The update shows there are short-term pressures: rising costs, a more cautious consumer, and patchy weather patterns have all contributed to a weaker margin outlook.

The company reports interim results on 29 July.

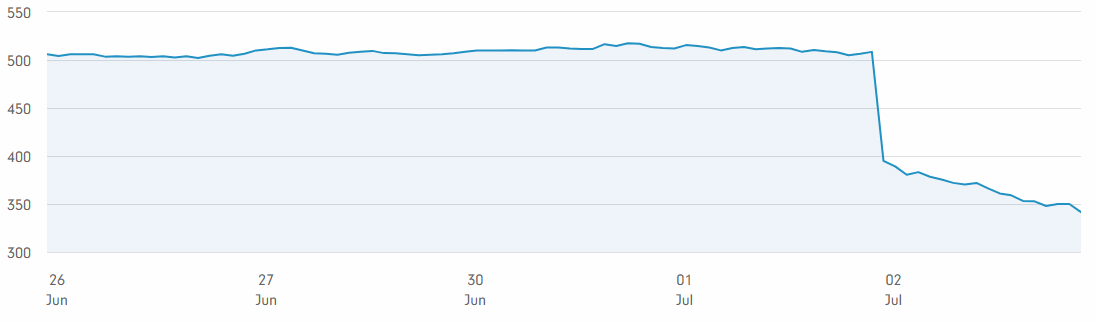

Bytes Technology Group plc - 31.52% (02/07/2025)

P/E Ratio: 23.96

Price/Book: 12.51

Dividend (Yield): 5.85%

EPS: 0.23

Trading Headwinds

Bytes reported a slower start to the financial year, with trading impacted by macroeconomic uncertainty and deferred buying decisions—particularly in the corporate sector. These pressures were flagged at the final results and have persisted into the first half.

The company also noted the near-term impact of changes to Microsoft’s enterprise incentive structure. These changes have been felt more in the first half, coinciding with key public sector renewals in March and April, and Microsoft’s fiscal year-end in June. While services revenue is growing, profit recognition is spread over the life of the contracts, meaning the full benefit builds gradually across the year.

Bytes now expects gross profit in H1 FY26 to be broadly flat year-on-year, with operating profit coming in slightly lower.

Sales Team Overhaul

In line with its strategic focus on customer centricity, Bytes has reshaped its corporate sales division—moving from a generalist setup to specialist teams targeting defined customer segments. This transformation has taken longer to bed in than expected, but management believes it will drive stronger engagement and more sustainable annuity-style income over the longer term.

It’s a shift that comes with some disruption upfront but could strengthen the business model if successful.

Despite the tougher backdrop, Bytes continues to invest in its front-line sales teams, aiming to stay competitive in a market where relationships and technical knowledge are key. The rest of the business is being run with more caution to maintain flexibility should conditions improve later in the year.

My thoughts:

Bytes is a company I have owned in the past. Years ago, while screening stocks, I discovered Bytes and turned a 30% profit within a matter of months. With the recent news and the share price low again, I’m planning to take some time to dive back into Bytes and try to properly value the shares.

Thank you for reading.

Let me know if you’d like to see a deep dive on Greggs or Bytes!

The information provided in this article is for informational purposes only and represents my personal opinions and analysis. It should not be construed as financial advice or a recommendation to buy or sell any securities. Investing in the stock market carries risks, and past performance is not necessarily indicative of future results. Readers are strongly encouraged to carry out their own research and seek advice from a qualified financial advisor before making any investment decisions. I do not accept any responsibility for any financial losses or consequences that may arise from reliance on the information presented in this article.