Buy Now, Regret Later?

Klarna’s Rise in the Wild West of Borrowing — and the UK’s BNPL Crackdown

A Premium Subscription Gets You:

✅ Exclusive market commentary

✅ FTSE-focused deep dives

✅ Actionable trade ideas

✅ Monthly portfolio insights

✅ Direct access & subscriber-only discussion

Dear Reader,

This week, I want to talk about something I’ve been seeing more and more — and it’s a bit worrying.

Buy Now, Pay Later schemes are everywhere. Klarna is the biggest name, but even PayPal has jumped on board. You’ve probably noticed the options at checkout — “Pay in 3,” “Spread the cost,” “No interest.” It sounds harmless enough.

I’m not against BNPL — it can be useful if you need to spread the cost over a few months. But what concerns me is the lack of proper regulation and the grey area these companies operate in. It’s all too easy for people to slide into debt without realising it.

In this piece, I’ll look at how changing habits are driving the growth of companies like Klarna, some worrying stats on BNPL, the risks if you miss payments, and what the UK government is doing to try and tighten things up.

On the face of it, it seems like a clever way to manage your money. Why pay all at once when you can split it over a few months?

But here’s the catch. “One in ten BNPL users has been chased by debt collectors for missed payments”. Klarna’s default interest rate is nearly 19% — on par with credit cards. And if you do miss a payment, it’s not just a slap on the wrist — your credit score can take a hit, which could affect your chances of getting a mortgage or even a phone contract.

Yet the advertising is all soft pastels and smiling faces. It doesn’t look or feel like borrowing — but that’s exactly what it is.

Changing Consumer Habits

Klarna is not targeting the wealthy who can afford these products, they are targeting the poorer members of society and then charging high interest rates when eventually someone does not pay on time! Its making people think they can afford these luxury items and entices consumer habits to overspend.

If you're 18, maybe working part-time — like I was back in the day, earning just under £5 an hour — it’s easy to see the appeal of buy now, pay later schemes. The psychology is simple: it doesn’t feel like you’re spending much when you split the payment over three months. Suddenly, buying something you normally couldn’t afford seems doable.

^A good example is Klarna’s partnership with JD Sports, whose core customer base typically falls between the ages of 16 and 24.

And while we can argue this encourages people to skip the old-school “save now, buy later” mindset (which is still incredibly important), that’s not really where Klarna and others make their money. As mentioned earlier, it’s not the majority who pay on time that keep the lights on — it’s the ones who don’t. Those who miss payments and get hit with interest rates of up to 18.9% are where a lot of the profits come from.

Research is starting to show just how much BNPL is changing the way people shop. A study by Imperial College Business School found that:

“BNPL instalments increase customer spending — both in how often people buy and how much they spend. By reducing the perceived cost and increasing the sense of budget control, BNPL actually makes people feel like they’re managing their money better, even when they’re spending more.”

It’s a clever business model — no doubt about that. And for many consumers, it does offer flexibility. But the stats speak for themselves:

69% of BNPL users admit they used it even though they originally planned to pay in full.

Over half of BNPL users have at least one outstanding payment, and half of those owe more than £100.

1 in 5 users are now using BNPL to cover essentials — like groceries or household bills.

Klarna isn’t targeting wealthy shoppers who could easily afford to pay outright. They’re targeting people lower down the income scale — people who are more likely to feel the squeeze and more vulnerable to missed payments. They’re selling the illusion of affordability while charging high interest when things go wrong.

It’s creating a culture where people are nudged into thinking they can afford luxury items — when in reality, they’re being pulled into a cycle of over-spending and quiet debt.

UK Government will start regulating BNPL firms.

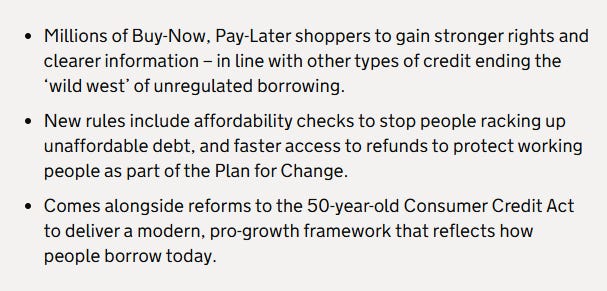

After years of delays, the UK government is finally moving to regulate Buy Now, Pay Later (BNPL) firms like Klarna, bringing them under the control of the Financial Conduct Authority (FCA). Until now, these companies operated in a legal grey area—able to offer short-term credit without carrying out proper affordability checks or being held to the same rules as traditional lenders. Surprisingly, customers couldn’t even take complaints to the Financial Ombudsman Service (FOS), meaning there was no formal route to challenge unfair treatment. Under the new rules, that changes. Consumers will be able to raise complaints with the FOS and get refunds more easily, and BNPL firms will be forced to run more thorough checks on borrowers and be clearer in their advertising.

Emma Reynolds, Economic Secretary to the Treasury, said:

This marks a big shift for Klarna, which built its brand on smooth, frictionless spending. The new rules will likely slow things down—more paperwork, more oversight, and more customer protections. Klarna and others may need to rethink how they attract and approve customers, and the added compliance costs could eat into their margins.

Check out a great video by Martin Lewis on the new regulation:

Klarna Financials

Klarna's first-quarter 2025 financials reveal significant challenges beneath its growth narrative. The Swedish buy-now-pay-later firm reported a net loss of $99 million, more than double the $47 million loss from the same period last year. This increase is primarily due to a 17% rise in consumer credit losses, totaling $136 million .

Despite a 15% year-over-year revenue increase to $701 million, driven by a 33% surge in U.S. revenue , the company's profitability remains elusive. Adjusted operating profit stood at a modest $3 million, a slight improvement from a $2 million loss the previous year .

Klarna's aggressive expansion in the U.S., including partnerships with Walmart, DoorDash, and eBay, has exposed it to economic uncertainties, leading to the postponement of its planned U.S. IPO . The company's funding costs also rose by 15% year-over-year to $130 million, further straining its financial position.

^DoorDash is the US equivalent of Deliveroo—once again encouraging people to overspend, this time on takeaways!

While Klarna boasts 100 million active consumers and over 724,000 merchants, the increasing credit losses and rising operational costs suggest that its business model may not be as sustainable as portrayed. The reliance on consumer debt and the challenges in repayment underscore the potential risks for consumers enticed by the allure of interest-free payments.

^Interesting video on how Klarna’s CEO wants to reshape the company’s image into a Neobank. Is it just a delusion, or do you agree with the vision?

To Conclude

With new rules on the way, Klarna and other BNPL firms will have to change how they operate in the UK. What was once a fast and easy way to buy now and worry later will come with more checks and better protections for shoppers. For many young people, services like Klarna have made overspending all too easy. These changes won’t fix everything overnight, but they’re a step in the right direction.

Really curious to know your take on this — drop a comment below!

Thanks for reading,

Ollz

Sources and References:

https://bluesky-thinking.com/why-klarna-might-be-making-you-spend-more/

https://www.scotlanddebt.co.uk/articles/what-to-do-if-you-are-in-debt-to-klarna

https://www.gov.uk/government/news/new-rules-to-end-buy-now-pay-later-wild-west-protect-millions-of-shoppers-and-drive-growth

https://www.ft.com/content/6c4bf393-c80b-42b7-993a-35270143f688