Too the Moon and back

Navigating Challenges and Pursuing Growth: A Closer Look at Boohoo's Journey (LSE:BOO)

Dear reader

What a week it has been on the stock market and my attention was grabbed by Boohoo recently again!

Boo Hoo, what a stock its been. I always like reading about Boohoo, either in the news or on the forums. People seem to have such strong views on the brand both positively and negatively. And then It always seems to make headlines every few months with another issue either big or small!

This is one stock that was heading for the moon but came crashing back down to earth even faster. Join me reader as this article will take a look into Boohoo and hopefully leave you with some more ideas about the business and a better understanding.

Brands:

Lets start at the face of Boohoo. Boohoo has many brands with a wide range of demographics but mainly targeting teenagers and the younger generation. The aqasitions of brands like Karen Millen have allowed the buisness to expand their demographics to include now older ages.

Brands include:

BooHo

BooHooMAN

PrettyLittleThing

Nasty Gal

MissPap

Karen Millen

Coast

Oasis

Warehouse

Debenhams

Dorothy Perkins

Wallis

Burton

Acquisitions

Boohoo has been helped with their acquisition of some large brands.

With some very well know brands such as Burton that’s been around since 1903 and was acquired by Boohoo in 2021. They don’t just take on the name, they take on the history. But as we know reader, growth by aqasation is not always the best. Sometimes we want to see growth naturaly in their own brands.

Growth:

Boohoo acknowledges persistent challenges in its performance outlook. The company anticipates a decline in annual revenue for the fiscal year 2023/24, ranging from 12% to 17%. Simultaneously, the management envisions the adjusted EBITDA margin to be in the range of 4% to 4.5%.

In the initial half-year period, Boohoo foresees a notable decrease in sales by 10% to 15%, signaling a challenging start. However, optimism prevails as the company expects a rebound in the latter half of the fiscal year. To bolster operational efficiency, Boohoo has proactively implemented cost-cutting measures, exemplified by a substantial 36% reduction in stock levels over the past year. Additionally, the company is strategically investing in automation to streamline its business operations.

Over the past three years, the company has achieved significant market share gains, with a 43% increase in overall sales and a 61% growth in the UK market. Key accomplishments include the successful implementation of automation in Sheffield, resulting in operational excellence and substantial savings.

The upcoming launch of a US distribution center is expected to elevate the customer proposition. The company has optimized its inventory, reducing stock levels by 36% year on year. Strong cash generation and ample liquidity support ambitious growth plans.

Margin improvements are being reinvested to enhance the test and repeat proposition, emphasizing speed and competitive pricing. The medium-term outlook includes targeting an adjusted EBITDA margin of 6% to 8% and returning to double-digit revenue growth through scaling, cost optimization, and efficiency improvements.

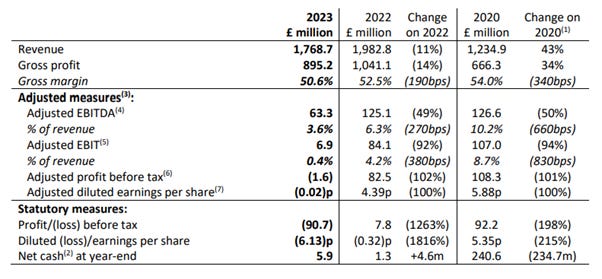

Financial Highlights for Full Year 2023:

· Revenue: £1.769 billion, down 11% from the previous year but up 43% compared to 2020.

· UK Revenues: Down 9% year-on-year but up 61% over the past three years, indicating significant market share gains.

· International Revenues: Down 13% from the previous year but up 22% compared to 2020.

· Gross Margin: 50.6%, reflecting a 190bps decline due to Covid-related cost pressures on raw materials, freight, and stock clearance.

· Inventory: Reduced by 36% year on year, totaling £101 million by the end of February.

· Adjusted EBITDA: £63.3 million, down 49%, with an Adjusted EBITDA margin of 3.6%.

· Capital Expenditure: £91 million invested in infrastructure for future growth, including Sheffield automation and a US distribution center.

· Cash Flow: cash generation, with a free cash flow of £30.2 million, driven by improvements in inventory and working capital.

· Balance Sheet: balance sheet with £136.1 million in unencumbered freehold assets, £5.9 million in net cash, and a £325 million Revolving Credit Facility, providing £331 million in liquidity headroom.

Most recent Half year Results from Boohoo:

Falls in Revenue and gross profit are bad indicators, but we are seeing a cost reduction plan in progress. Inventory falling means cost reduction will fall. I don’t like the look of the net cash/ (debt) position as I would want to see a company generating lots of cash and keeping some. Again, as this is half year 2024, I would be looking for the next half year to show some robust improvements

Profit margins and valuations:

The two graphs are not showing good news. There has been a decrease in the operating margin & EBITA margin which is why the valuation is decreasing. As those two fall the profitability of the business falls and thus shares will fall. We need to see a change in the profitability of the business and see growth like the good old days. If we can see this then the valuation will increase. But this is down to management to change this around. Boohoo is trying to get back to growth but dear reader the numbers don’t lie, and it will be interesting to see when they next report if they are starting to regrow.

Freasers Group

Let’s explore the famous Frasers who have been taking stakes in both Boohoo and ASOS recently. For people who read into this, what can it show?

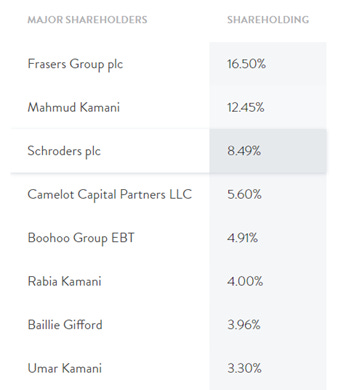

Frasers group who is controlled by Mike Ashley and own groups like Sports direct and House of Frasers keeps increasing their stake in Boohoo. Currently this has increase from 16.5% to 17.2% which is quite a large ownership of the company. Frasers Group became the biggest shareholder in Boohoo in October.

With the share price down so low, could this mean a takeover? Well reader I think the at prices like this they are seeing a real buy opportunity. If not, a takeover this is definitely a time where Frasers are increasing. It is worthy to note that Frasers are also buying Boohoos competitions ASOS as well.

Major ownership:

As of November 2023, what they are displaying on their website does show some large positions from some large institutions as well as owners. It is to note that Frasers group have increased their position

Problems

Let’s examine one problem that is affecting the share price and that is the Short positions.

Jan 2022, saw huge short positions coming in and at one point seeing it reach 10%. At one point this was one of the most shorted stocks on the market. Let’s further examine who is shorting Boohoo and see if their positions change as someone could argue the company is improving

Overall Short positions have fallen to 5.31%. Again, looking back at the history reaching 10%, this is a big fall. Looking further at the date change we can see Citadel have started to decrease their position where Ennismore Fund Management is increasing their positions. But reader, I would see the overall picture as the shorters are lowering their positions to what it was a year ago

More Problems?

Boohoo has grappled with significant challenges surrounding factory issues, particularly concerning pay and working conditions in their Manchester facility. The repercussions of these revelations in the past year had a notable impact on the company's share price, shedding light on subpar working conditions and low wages. Additionally, the potential closure of the Leicester factory is under consideration, but Boohoo has undertaken substantial changes, resulting in improved working conditions.

In a June report by Drapers, it was disclosed that Boohoo Group sought a 10% discount on current orders from specific suppliers, marking the second such request in two months. Furthermore, the company has asked for discounts exceeding 30% on outstanding orders from Turkish suppliers, aiming to align with the prices it has secured in Pakistan.

These actions indicate Boohoo's cost-cutting measures, potentially at the expense of sourcing goods from countries like Turkey and Pakistan. While this may positively impact cost reduction and competitiveness, it raises ethical concerns about the company's supply chain practices.

Another industry-wide challenge involves retailers charging customers for returns. This practice, adopted by major players like H&M, Zara, and Next, addresses the financial strain caused by a high volume of returns. Boohoo has discreetly implemented this approach, which, while discouraging bulk buying and excessive returns, could be advantageous for the company in managing costs effectively.

Are people leaving fast fashion?

This is a very big concern for the business but is it over blow? Well reader, I’m a little torn. On one hand we hear about how Gen Z are changing their buying habits and buying more sustainable. But then the numbers show business like Shien who are know for exploiting and cheap clothing are dramatically growing. So, from the numbers I’m less worried. I think the age of younger people with less money are more likely to buy. I’m not here to look into whether this is wrong or right, but clearly show how sales of fast fashion are not slowing down any time soon.

BOOHOO VS SHEIN

Despite emerging as the most downloaded shopping app in the US, Shein has deliberately kept a low public profile, a strategic move that sets it apart. Meanwhile, Boohoo is cautioning investors about a more significant-than-anticipated sales decline this year, attributed to consumers purchasing fewer items amidst robust competition from the Chinese competitor, Shein, and a resurgence of interest in high street shopping.

Shein's UK arm demonstrated remarkable success, generating over £1 billion in sales last year. Projections from GlobalData suggest that Shein is on track to solidify its position among the top 10 apparel firms in the UK by market share in 2023, underlining its growing influence in the industry.

25 day and 50 day moving Average

The chart shows Boohoos share price VS the 50-day moving average and the 25-day moving average. As we can see, Boohoo was hitting all-time lows of 0.30 in November and then started to climb back. Late November saw the 25-day moving average over the 50-day average and this is currently a positive sign

The End:

Boohoo grapples with financial hurdles as half-year 2023 results reveal a 17% revenue dip and adjusted EBITDA falling from £35m to £31m. Operating on a slim 4.3% margin, the company is susceptible to profit fluctuations.

Addressing the challenges, the management takes decisive action, cutting operating costs by 16% and closing the Leicester facility to trim long-term expenses. Boohoo, foregoing dividends, positions itself for growth.

Despite hitting a yearly low of 0.2777 p, the investment decision rests on confidence in Boohoo's turnaround potential. While acknowledging shortcomings, the company signals optimism for growth, echoed by Mahmud's proclamation at the interim results meeting.

Boohoo stands at a pivotal juncture, navigating financial challenges with a determined management team. Investors are urged to weigh the potential for improvement against market concerns, recognizing that strategic changes may pave the way for a brighter future.

I hope reader, this was a valuable insight into Boohoo. But remember always do your own research and everything here is my own opinion.

Ill leave you today with one of my favourite books and a good read into looking for clues a company is going to have a share price drop.

When companies suffer a dramatic even catastrophic drop in their share price, it is the investors who lose their shirts and employees their jobs. Tim Steer - The Signs Were There: The clues for investors that a company is heading for a fall

Thanks, O