Is Burberry (LON:BRBY) looking cheap?

A FTSE 100 Stock falling out of fashion?

Dear Reader,

Let's take a look at one stock that seems to have fallen out of fashion with investors and has come crashing down. Now trading at lower than its 5-year average and back at 2010 prices, I think it's time we take a little look at this FTSE 100 stock…

Financial Performance in FY24

Revenue and Sales:

Total Revenue: £2,968 million, a 4% decrease from £3,094 million in the previous year.

Comparable Store Sales: Down by 1%, compared to a 7% increase the prior year.

Profitability:

Adjusted Operating Profit: £418 million, a 34% decline from £634 million, with a corresponding profit margin drop from 20.5% to 14.1%.

Reported Operating Profit: Fell by 36% to £418 million, with the margin decreasing from 21.2% to 14.1%.

Adjusted Diluted EPS: Dropped by 40% to 73.9 pence.

Reported Diluted EPS: Down by 41% to 73.9 pence.

Cash Flow and Dividends:

Free Cash Flow: £63 million, an 84% reduction from £393 million.

Proposed Dividend: 61.0 pence, remaining flat compared to the previous year.

Regional Sales Performance

Group Sales: Declined by 12% in Q4 but only 1% for the full year.

Asia Pacific: Faced a 17% decline in Q4 but grew 3% for the year.

EMEIA: Improved by 4% annually, despite a 3% drop in Q4.

Americas: Saw a consistent 12% decline both in Q4 and FY24.

Strategic Progress in FY24

Burberry has made significant strides in several key areas:

Brand and Product Evolution: Focused on storytelling around Modern British Luxury, resulting in improved brand perception and double-digit growth in elite customer numbers and spending.

Aesthetic and Quality Enhancements: Elevated the design and quality of seasonal collections, beginning reinvigoration of larger core collections.

Distribution Network Strengthening: Over 50% of stores are now new or refurbished.

Supply Chain Reconfiguration: Adapted to new creative visions, improving product availability and strengthening manufacturing capabilities, while continuing sustainability initiatives.

Priorities for FY25

Looking ahead, Burberry has set clear priorities to navigate the uncertain environment:

Brand Refinement: Enhance brand expression and product storytelling, and deepen client engagement.

Product Offer Expansion: Balance seasonal and core collections.

Retail and Online Experience: Improve in-store experiences and online customer interactions, and rationalize the wholesale channel in EMEIA for better distribution control.

Operational Efficiency: Drive cost efficiencies and advance sustainability efforts.

Outlook

Despite an uncertain external environment, Burberry expects challenges to persist into the first half of FY25, with anticipated benefits from strategic actions manifesting in the second half. The company estimates a 25% reduction in wholesale revenue in H1 as it gains more control over distribution. Cost savings have been identified to mitigate inflation impacts in H2. Burberry also anticipates a currency headwind of approximately £30 million to revenue and £20 million to adjusted operating profit based on current exchange rates.

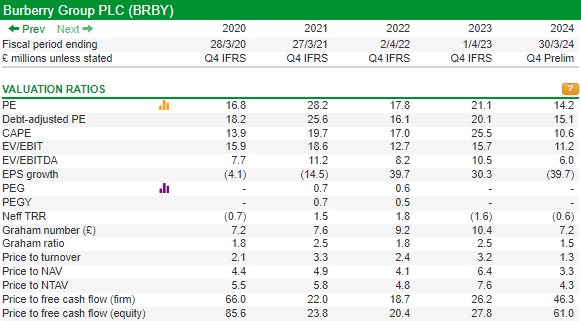

*Key Financial Data

Burberry's Dividend Strategy

Burberry Group plc (LON: BRBY) has announced a dividend of £0.427 per share, payable on the 2nd of August. This translates to an annual yield of 5.7%, which is notably higher than the industry average.

Dividend Coverage: Despite a historically high payout ratio, Burberry's dividend remains well-covered by earnings and cash flows. Currently, the dividend consumes 73% of free cash flows, suggesting sustainability and sufficient funds for reinvestment.

Future Prospects: With earnings per share (EPS) forecasted to grow by 17.4% next year, the payout ratio is expected to remain manageable at around 72%, supporting future dividend payments.

Dividend Volatility and Growth

While Burberry boasts a long history of dividend payments, the dividend has been cut at least once in the past decade. From an annual payment of £0.29 in 2014, it has grown to £0.61 recently, averaging an annual growth rate of about 7.7%. Despite this growth, the past cuts highlight some volatility in dividend stability.

Growth Prospects: Earnings per share have not significantly changed over the past five years, indicating limited growth prospects. However, the recent stability in dividend payments and sufficient cash flow coverage provide a degree of reliability.

Shorts:

Short postions by Marshall Wace LLP & Millennium International Management LP total 3.21%. This is affecting the share price but can it go on much longer if management are able to turn this ship around?

Conclusion

Pros:

Attractive dividend yield with good coverage.

Strategic initiatives aimed at brand enhancement and operational efficiency.

Trading at historically low prices, potentially offering a buying opportunity.

Cons:

Significant recent declines in revenue, profit, and cash flow.

Uncertainty around market recovery and regional sales performance.

Historical dividend volatility and limited recent EPS growth.

Given the mix of attractive dividends and strategic initiatives versus significant financial declines and market uncertainties. I am cautious about investing in this stock

I don’t hold Burberry (yet?), but I’m definitely tempted by what I see. I think there are a lot of factors in play at Burberry and they still need to make improvements. However, it’s still a profitable company trading at 2010 prices.

This stock is a falling knife, and where the bottom is, I’m not quite sure. The problem with a falling knife is trying to catch it without getting cut!

Over the coming weeks, I think it will be interesting to watch the share price and maybe take a little dip at the right price.

Let me know what you think and if you hold Burberry!

Remember, this is not financial advice and purely my own opinion. You must do your own research.