How Britain Lost Its Gold

The Great Gold Sell-Off: What Really Happened Under Gordon Brown

Dear reader,

A Sale That Still Raises Eyebrows

If you were watching markets at the turn of the millennium, you’ll remember it. Between 1999 and 2002, Gordon Brown — then Chancellor of the Exchequer — sold off nearly 400 tonnes of Britain’s gold reserves. It was a decision met with confusion and criticism at the time, and one that has aged poorly.

The rationale? Diversification. The execution? Flawed. The timing? Disastrous.

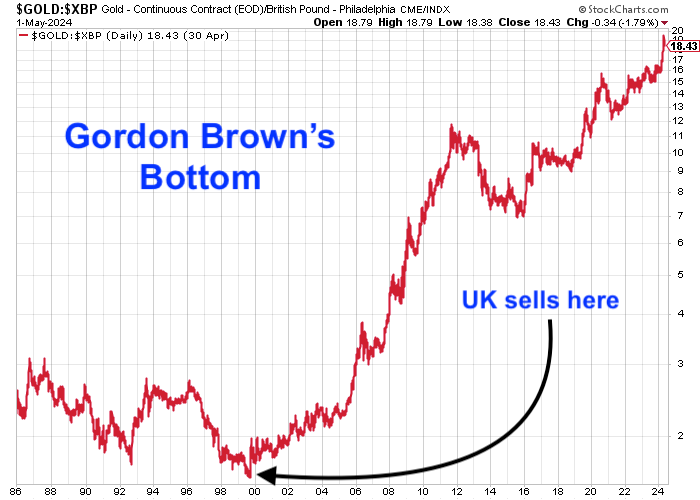

The gold was sold at an average price of around $275 an ounce — the lowest point in over two decades. Worse still, the Treasury telegraphed its intentions to the market, pushing prices even lower before the first bar had left the vault. In total, the UK gave up around half its gold reserves — just before gold entered a bull market that would see it rise sevenfold over the next decade.

This wasn’t just bad luck. It was a fundamental misreading of gold’s role as a long-term store of value and a hedge against monetary excess.

This article takes a closer look at how it happened — and why it remains a textbook example of what not to do with national assets.

Image from: https://www.bbc.co.uk/news/business-39178988

Why Did the Treasury Sell the Gold?

At the time, Gordon Brown said the sale of Britain’s gold reserves was about “modernising” the portfolio. Gold, he argued, had underperformed for years, and it made sense to switch into more modern assets — like US dollars, euros and yen — that paid interest and could be more actively managed.

On the surface, it sounded logical. But scratch beneath it, and the decision doesn’t hold up.

Yes, gold was unloved in the late 1990s. It had gone nowhere for years, and many thought it had had its day. But investing isn’t about chasing what’s worked recently — it’s about holding on to what will protect you when the tide turns. Gold’s role wasn’t to produce income. It was to act as a safety net — a hedge against inflation, currency risk, or financial shocks. None of that had gone away.

Instead of waiting for sentiment to turn, the Treasury gave up nearly half the UK’s gold just as the world economy was about to shift. Within a few years, gold was surging as inflation fears returned, the US dollar weakened, and trust in central banks wobbled. The UK, meanwhile, had swapped its gold for low-yielding foreign bonds — the same kind of assets that would later come under pressure in the global financial crisis.

To make matters worse, the gold was sold publicly and in stages, giving the market plenty of time to drive the price down even further. It was like telling everyone you’re about to offload a classic car collection — and then acting surprised when buyers offer lowball prices.

Other countries, including China and Russia, quietly went the other way. They increased their gold holdings, recognising its long-term role as a store of value and a hedge against Western debt and currency exposure.

Image from: The Flying Frisby, https://shorturl.at/EX9Wt

What Happened Next

The timing of the sale couldn’t have been worse. After hitting rock-bottom in 1999 at around $250 an ounce, gold began a steady climb — and by 2011, it had reached nearly $1,900. That’s more than a sevenfold increase.

Had the UK held on to those reserves, the country would have benefitted from one of the strongest commodity bull runs in modern history. Instead, the Treasury missed out on an estimated £10–13 billion in potential gains — money that could have been used to shore up public finances during the financial crisis or reinvested elsewhere.

Even more damning is how the policy is now viewed. What was once sold to the public as prudent financial management is widely seen — even within Labour circles — as a major economic blunder. Ed Balls, one of Brown’s closest allies and a key Treasury adviser at the time, has since admitted the political damage it caused and the regret felt over the outcome.

Was Gold Really That Unattractive in the 90s?

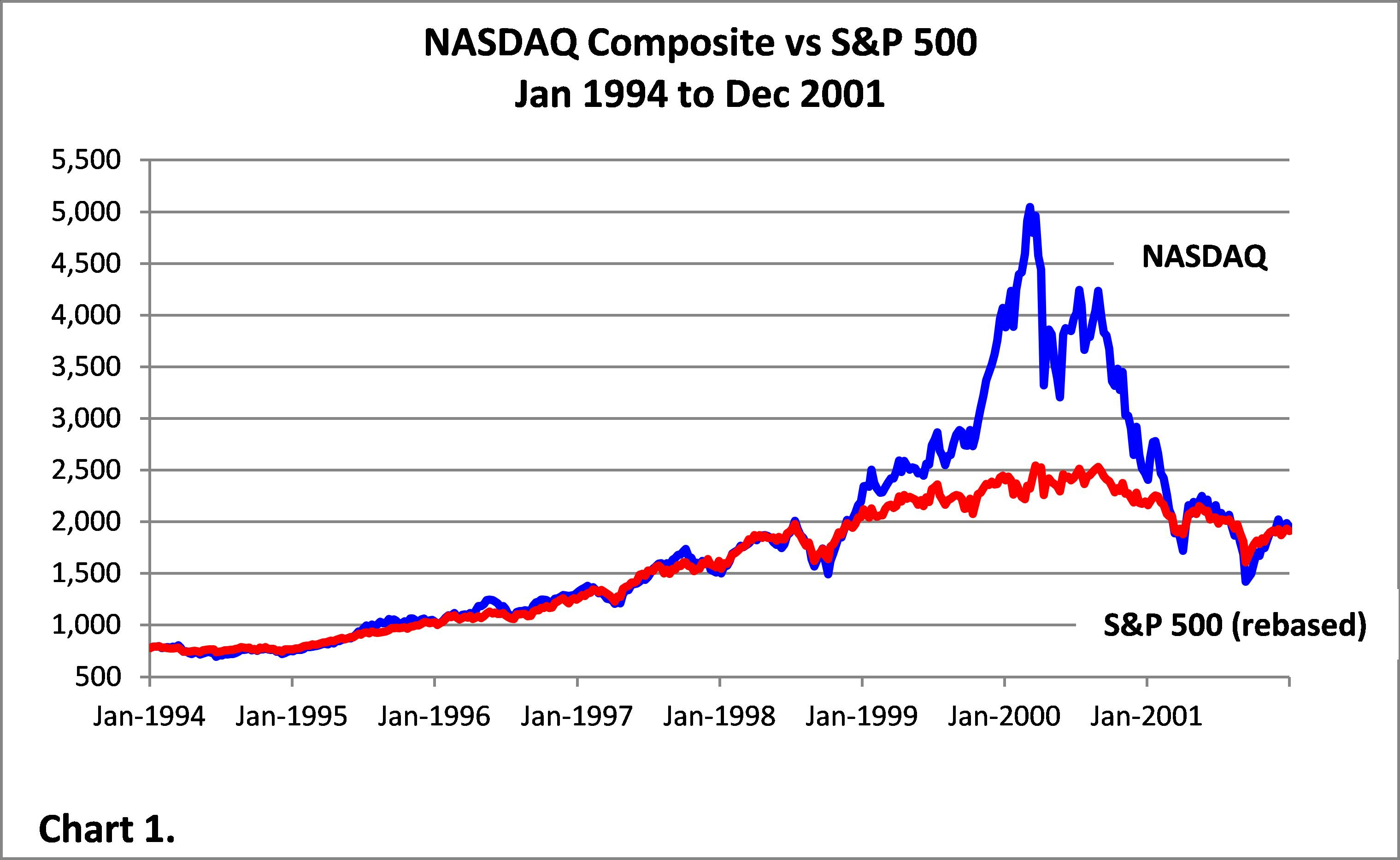

In the late 1990s, gold was deeply out of favour. With inflation firmly below 3%, soaring tech stocks, and a robust U.S. economy, gold was routinely dismissed as a relic. It traded in a tight $300–$400 band throughout most of the decade, plunging to as low as $252 per ounce by mid-1999—its lowest level in two decades

Central banks joined the chorus—many were quietly trimming their gold holdings, contributing to oversupply and further depressing prices. Gordon Brown’s announcement in May 1999 sent a clear signal: the UK didn’t just lack conviction in gold—it was actively unloading it. That public declaration alone drove prices down approximately 10% by July, before the first official sale occurred.

Yet beneath this consensus lay the seeds of a major miscalculation. The turn-of-century calm disguised a brewing storm—dot-com volatility, geopolitical shocks, and eventually ballooning fiscal deficits. Gold’s role had never been about fitting in with the economic fashion of the day, but about offering insurance when that fashion inevitably unraveled. The Treasury’s justification—diversification into low-yielding fiat bonds—missed the point entirely. Gold doesn’t bear interest because its value resides in its resilience, not in coupon payments.

Image from: https://shorturl.at/3RatI

Conclusion

Gordon Brown’s decision to sell nearly half of Britain’s gold reserves is now widely regarded as one of the worst financial decisions in modern UK history — and rightly so. Wrapped in the language of modernisation and diversification, the move was anything but forward-thinking. It was reactive, poorly timed, and rooted in a fundamental misunderstanding of gold’s role in a national reserve strategy.

Instead of protecting against risk, the UK government offloaded its most durable hedge at the bottom of a decades-long cycle — swapping permanence for yield, security for fashion. The fact that the sale was announced in advance, encouraging front-running and further depressing the price, only compounded the damage. It wasn’t just bad luck. It was a failure of judgment, execution, and economic foresight.

While others quietly bought gold, recognising its strategic importance, Britain sold. And when the global economy faltered — through dot-com collapse, war, and financial crisis — the safety net was already gone. The result? Billions in lost value, and a generation of policymakers left defending the indefensible.

Thanks for reading,

Ollz

Sources and further reading:

https://auronum.co.uk/the-browns-bottom-gold-sale/

https://www.bullionbypost.co.uk/gold-news/2019/may/07/worst-deal-uk-history-20-years-brown-sold-britains-gold/

https://goldbullionpartners.co.uk/the-gordon-brown-gold-reserves-myth-what-really-happened/

https://www.proactiveinvestors.co.uk/companies/news/1046585/gordon-brown-s-gold-sale-spectre-still-haunting-after-25-years-1046585.html

An education for those of us that weren’t even born!

I remember the act of folly, Brown was a die hard socialist and never understood the store of value concept