Goodbye Schroders

The End of an Era on the FTSE 100

Dear reader,

A more personal article for me today… My first job was with Schroders, and I spent several years there. It wasn’t just the work itself that made it a great first job it was the people. The teams, the culture, the way everyone worked together it really set the tone for my career.

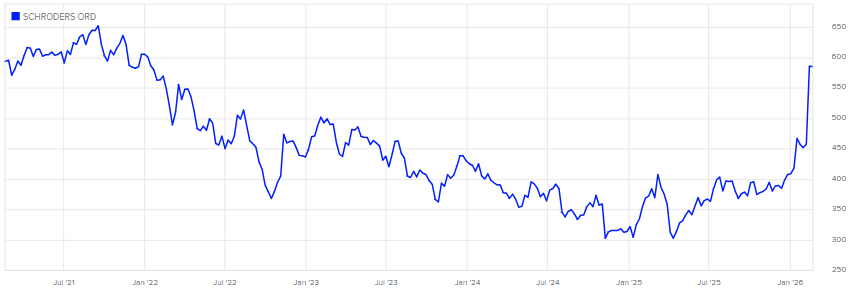

Now, fast forward to today, and we’re looking at Schroders being bought out by Nuveen, the US asset manager. It’s a big deal. We’re talking a £9.9 billion takeover, with Schroders’ shares jumping nearly 30 % on the news. Once the deal goes through later this year, Schroders will delist from the London Stock Exchange and leave the FTSE 100. For anyone who’s followed the company, it’s a huge moment the end of a chapter that’s been 220 years in the making.

What This Means for Schroders

For Schroders itself, the deal is a strategic response to the pressures facing mid-sized active managers. Global competition has intensified, larger US rivals dominate scale, technology, and distribution, and fee compression has made growth harder to achieve independently. Joining Nuveen gives Schroders access to a larger international platform, more resources, and the ability to compete on a global stage.

The Schroders brand and London offices will continue, and the team is expected to remain largely intact. But independence is gone, and decisions that were once taken in London will now be part of a global corporate structure.

Implications for the FTSE

Schroders leaving the FTSE 100 is another example of a trend that has been quietly accelerating: long-established UK companies being bought out or taken private. Other recent examples include:

Darktrace – The cybersecurity company, once a high-profile “unicorn” on the London Stock Exchange, was acquired by US private equity firm Thoma Bravo for approximately $5.3 billion. Following the deal, Darktrace was delisted, removing one of the fastest-growing UK technology names from public markets. Its exit highlights the challenges UK tech firms face in maintaining long-term domestic listings amid global investor appetite.

Hargreaves Lansdown – The UK’s largest retail investment platform, managing over £150 billion in client assets, agreed to a £5.4 billion buyout led by a consortium including CVC Capital Partners, Nordic Capital, and the Abu Dhabi Investment Authority. Once delisted, this transaction took another household UK financial brand out of public ownership, underscoring how private equity is reshaping the structure of UK financial services.

TI Fluid Systems – A FTSE 250 supplier of automotive components, TI Fluid Systems was acquired for around £1 billion by Canadian firm ABC Technologies, backed by Apollo Global Management. This takeover included plans to delist from the London market, highlighting that even mid-cap industrial companies are not immune to foreign acquisition pressures.

Arm Holdings (historic but instructive) – Perhaps the most high-profile example, Arm, a UK technology champion, was acquired by SoftBank and delisted from the London Stock Exchange before later relisting in the US. Arm’s journey demonstrates how UK-grown global leaders can drift away from domestic markets, depriving local investors of stakes in world-leading businesses.

What Schroders Offers

From Nuveen’s standpoint, the logic is straightforward. Schroders brings a long-established brand, institutional relationships and investment capability at a valuation the market had struggled to sustain. The premium offered reflects less a sudden improvement in prospects than a reassessment of ownership.

Schroders was not a distressed asset. It remained profitable and operationally sound. Its challenge was structural. Mid-sized active managers have found it increasingly difficult to convince public markets of their growth potential amid fee pressure, the rise of passive investing and the scale advantages enjoyed by larger US groups.

The consequence is a recurring pattern. Businesses that generate steady cash flows but lack a clear growth narrative trade at persistent discounts. Those discounts invite acquisition. The departure of another constituent from the FTSE 100 is therefore less a shock than a continuation of a well-established trend.

Not an Isolated Case

Schroders’ exit fits a broader pattern that has become difficult to ignore. UK-listed companies with durable franchises but modest growth profiles have increasingly found themselves valued more highly by private or overseas buyers than by domestic public markets.

In part, this reflects structural features of the UK market itself. Pension funds have continued to reduce equity exposure, retail participation has waned, and the investor base has tilted towards income and near-term returns. That combination has tended to favour yield over reinvestment and stability over ambition.

For companies operating in capital-intensive or highly competitive global industries, the result is often a persistent valuation discount. Over time, that discount becomes self-reinforcing: management teams focus on cost control and capital discipline rather than expansion, which in turn limits the growth narrative investors are seeking.

Against that backdrop, takeover interest is not an anomaly but an outcome. For buyers with longer time horizons or different return requirements, the arithmetic simply works. For the London Stock Exchange, it is another reminder that competitiveness is measured not only by listings won, but by those retained.

What, If Anything, the Government Can Do

The UK government is not powerless in this process, but neither does it have a simple lever to pull. Takeovers such as this one are a symptom of deeper capital-market dynamics rather than regulatory oversight failures.

That said, policy choices matter at the margin.

A starting point would be addressing the domestic investor base. UK pension funds remain structurally under-allocated to equities, particularly domestic ones. Encouraging long-term institutional capital back into listed UK companies whether through reform of defined-contribution defaults or incentives for productive finance would help narrow persistent valuation discounts. Much of this sits with HM Treasury, rather than company regulators.

Listing reform is another area where progress has been uneven. While changes to free-float requirements and dual-class share structures have helped at the margin, they do little for established companies whose issue is valuation rather than access. Liquidity, analyst coverage and depth of capital matter more than rulebook flexibility once a company is mature.

There is also the question of stewardship. The UK has been effective at attracting overseas buyers but less successful at retaining domestically listed champions. Industrial policy has tended to focus on innovation and start-ups, leaving scaled incumbents exposed to global capital flows without corresponding domestic support.

None of this implies that UK Government should block deals or protect companies from acquisition. But if the repeated exit of long-established firms is viewed as a problem rather than a market outcome the response lies in making public ownership more competitive, not more defensive.

Absent that, transactions like Schroders’ will continue to look less like exceptions and more like the natural endpoint of a UK listing.

Thanks for Reading,

Ollz

Sad end to an era being acquired by the Americans, at this rate FSTE will become a satellite to the S & P

Your reasoning for saying goodbye to Schroders was really thoughtful what’s one lesson from that decision you think other investors often overlook?

I supported your work I’m building my own Substack right. Let’s support each other; feel free to check mine out too.