Dear reader,

B&M is one of the stocks I’ve written about most on my Substack—and for good reason! It’s a very interesting company.

I like it for many reasons, and I’ll name a few. B&M is a discount retailer that offers competitive prices compared to the likes of Sainsbury’s, Tesco, and M&S. While it doesn’t directly compete with these supermarkets, we’re seeing a broader shift in the UK towards more affordable options like ALDI and LIDL. However, B&M is a little different—it offers discounted groceries, household goods, and homeware, and still competes with the likes of The Range and B&Q. With such a wide mix of competitors, B&M has more opportunities to grab market share. Just look at how ALDI and LIDL entered the UK market and have quickly disrupted the grocery sector in recent years. I know I’ve found myself shopping at ALDI more often than Sainsbury’s!

But enough about me. The financials for B&M are compelling—especially against a backdrop of what feels like constant bad news. Perhaps the most widely known headline is that B&M recently dropped out of the FTSE 100 and is now part of the FTSE 250.

I’ve taken a snip from MarketBeat to show how B&M is currently priced compared to its competitors:

With their most recent results released on June 4th, I want to take a deeper dive into several aspects—examining the financials, growth, and market positioning—to see if B&M still looks undervalued and worth buying at today’s price.

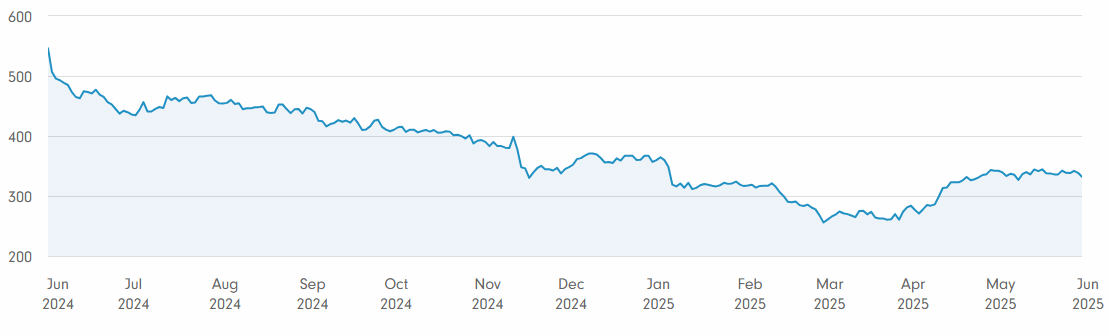

B&M 5 yr chart:

Keep reading with a 7-day free trial

Subscribe to Going Long to keep reading this post and get 7 days of free access to the full post archives.